For many retirees, Social Security isn’t just a monthly deposit — it’s a lifeline. It generally replaces about 40% of the average worker’s pre-retirement income. That’s a good start, but it leaves a big question: Where’s the other 60% going to come from? That’s why when — and how — you claim benefits can make a major difference in your retirement income strategy.

Understand the 40% Rule (and the Missing 60%)

The average retiree’s Social Security check covers ~40% of prior income. The rest usually comes from:

- Retirement savings — 401(k), IRA, brokerage.

- Pensions — more common in public sector/union roles.

- Part-time work — income + purpose.

- Other sources — annuities, rentals, small business income.

Quick tip: Calculate your “income gap” early so you can plan how to fill it. Our Social Security Filing Strategy Worksheet will walk you through it.

Filing Age Matters More Than You Think

You can start collecting as early as 62 or delay up to 70. Your Full Retirement Age (FRA) is usually 66–67 depending on birth year.

- Claim early (62–FRA): Smaller monthly check for life.

- Claim at FRA: Receive 100% of your calculated benefit.

- Delay past FRA (to 70): Benefit grows ~8% per year you wait.

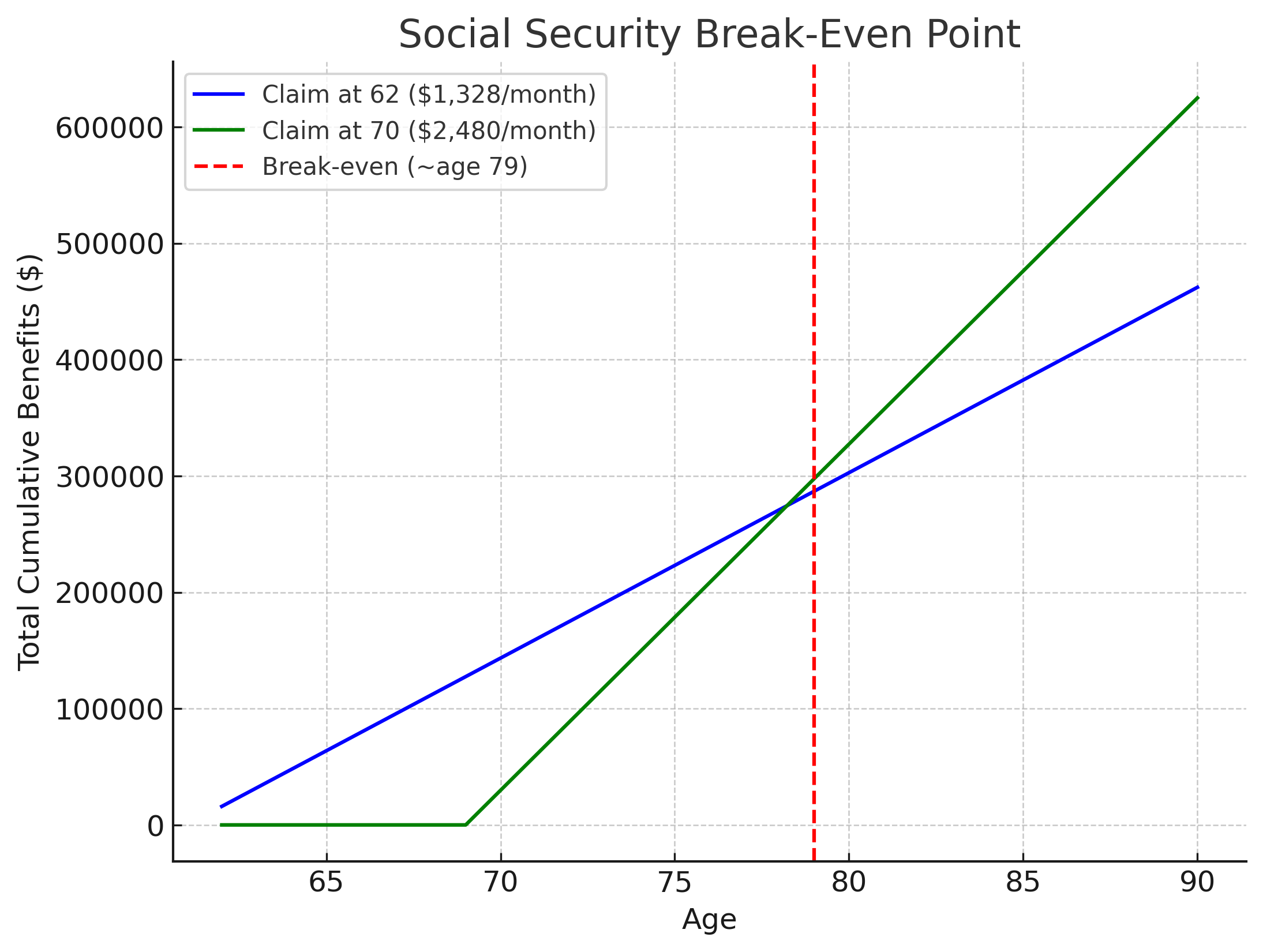

The Early vs. Delayed Break-Even Point

If you claim early, you collect sooner but at a reduced amount. If you wait, your monthly check is larger but you’ll receive fewer payments overall. The break-even age is when the total you’ve received by delaying overtakes the total you’d have received by filing early.

Here’s the concept of the break-even chart:

- Most people find the break-even age is somewhere between 78–82.

- If you expect to live well beyond that, waiting can mean more lifetime income.

- If your health is uncertain, earlier filing can make sense.

Spousal & Survivor Benefits You Don’t Want to Miss

- Spousal benefits: A spouse can claim up to 50% of your benefit at their FRA (based on your record).

- Survivor benefits: A surviving spouse can receive up to 100% of the deceased spouse’s benefit if higher.

- Divorced spouse benefits: If you were married ≥10 years and aren’t remarried, you may qualify.

Coordinating filing ages between spouses can meaningfully change lifetime income. Sometimes one spouse files earlier while the other delays for a higher survivor benefit.

Run the Numbers Before You File

Model different claiming ages with the SSA calculators, then layer in your other income sources to see your full cash-flow picture.

Related Reading on Senior Town Hall

- Figure the Figures – How Much Money Do You Need to Retire?

- Estate Planning: Dignity, Control, and Protecting Loved Ones

- Long-Term Care: Understanding the Costs and Coverage Options

Disclaimer: The information provided here is for educational purposes only and should not be taken as financial, legal, or tax advice. Consult with a qualified advisor before making any Social Security or retirement decisions.

New to Medicare? Start Here.

Parts A–D, what’s covered vs not, enrollment windows, and common penalties—explained simply.

Educational only. The information on seniortownhall is provided for general educational purposes and is not financial, legal, tax, medical, insurance, or investment advice. Rules (e.g., Social Security, Medicare, tax law) change frequently and may have changed since publication.

Please consult a qualified professional who can consider your individual circumstances before acting on any information.

© 2026 seniortownhall. All rights reserved.