“You don’t want to run out of money before you run out of sunshine.”

It’s a bit blunt, but it captures the number-one fear in retirement: outliving your money. The way you prevent that isn’t luck or guesswork — it’s balance. In investing terms, that balance is called asset allocation.

Asset allocation is simply how you divide your money across different income sources and investments. It’s about making sure no single piece of your plan carries all the weight.

Level One: The Three Key Sources

Forget the old “three-legged stool” of Social Security, pensions, and savings. Most retirees today don’t have pensions — and that model doesn’t fit. Instead, think of retirement income in three broad categories:

1. Social Security – The base for almost everyone. Covers about 40% of income needs on average, guaranteed for life.

2. Retirement Accounts – 401(k)s, IRAs, 403(b)s. Usually the largest pool of savings.

3. Other Investments & Assets – Brokerage accounts, real estate, rental income, insurance products.

For some, Social Security is the anchor. For others, investments and savings outweigh it. Either way, your job is to balance these sources so you don’t lean too heavily on just one.

Walking Through the Math

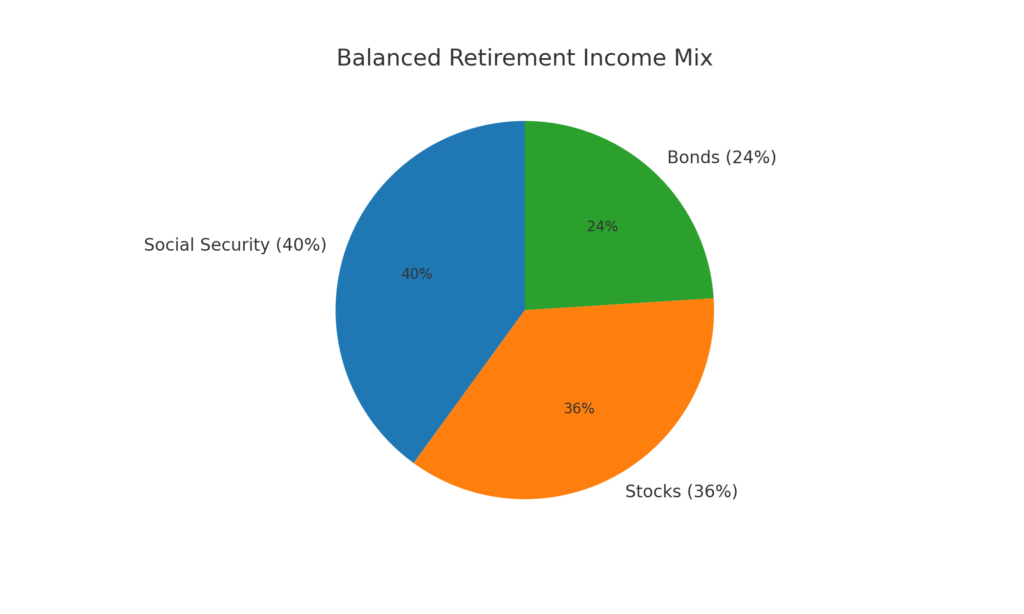

Here’s a simple framework that shows how the balance works:

– Social Security covers 40% of your needs.

– That leaves 60% to come from savings and investments.

– Apply the 60/40 rule to that 60%:

• 36% from stocks (growth)

• 24% from bonds (stability)

That gives you a Balanced Mix:

Level Two: Inside Your Savings

Once you’re looking at your personal savings, allocation is about dividing among:

– Stocks → higher growth, higher ups and downs.

– Bonds → steady income, less volatile.

– Cash equivalents → safe and liquid for short-term needs.

Other supports like home equity or part-time work can fit here too, but stocks, bonds, and cash are the “core mix.”

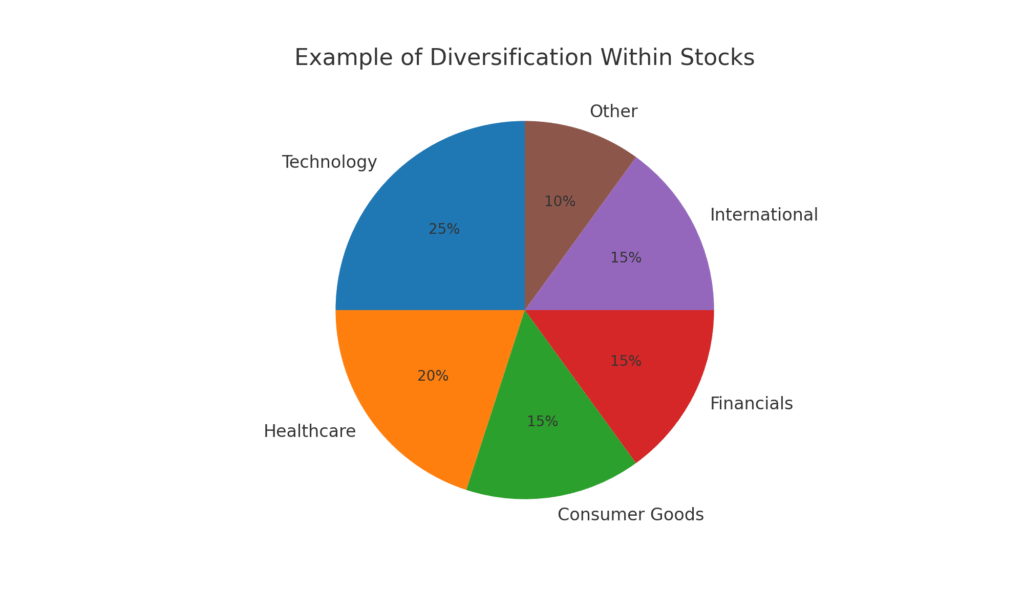

💡 Note: Even within stocks, you’ll hear about different allocations — like technology vs. healthcare, U.S. vs. international, growth vs. value. These categories help spread risk and opportunity. For most retirees, though, this is where mutual funds and ETFs do the heavy lifting.

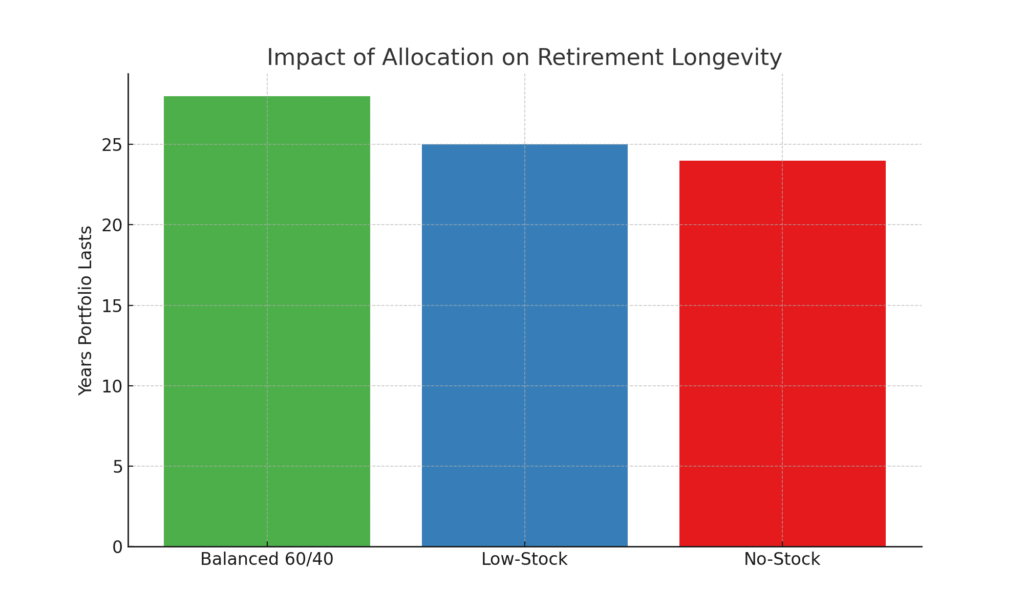

What Happens If You Don’t Invest in Stocks?

It’s tempting to say, “Stocks are too risky — I’ll just keep my money in bonds.” But here’s the trade-off: without growth, your money may not last as long.

Here’s a simple comparison, using long-term average returns:

Strategies to Keep You Balanced

1. The 60/40 Portfolio

60% stocks, 40% bonds (applied to your investment bucket).

Classic model: balances growth with stability. Still useful, but may need adjusting for your age, risk tolerance, and income needs.

2. Target-Date Funds

A sliding scale of risk, not income.

• Heavy in stocks when you’re younger (more risk, more growth).

• Gradually shifts into more bonds as you near retirement (less risk, less chance of a crash late).

• Example: a 2035 fund assumes you’ll retire in 2035 and automatically rebalances as you approach.

3. The Bucket Strategy

This approach divides money by time horizon:

– Bucket 1: Short-Term (1–2 years) → Cash, CDs, savings accounts.

– Bucket 2: Medium-Term (3–7 years) → Bonds or bond funds.

– Bucket 3: Long-Term (8+ years) → Stocks or stock funds.

When you need money, you draw from Bucket 1. When it runs low, you refill it with interest from bonds or harvested growth from stocks. This prevents you from selling stocks during a downturn to cover bills.

The Takeaway

– Social Security provides your foundation, but only about 40%.

– Retirement accounts and investments must fill the gap.

– Asset allocation is how you keep that balance steady.

– The right mix reduces the odds of running out of money before you run out of sunshine. 🌞

⚠️ Disclaimer: These are simplified illustrations using historical averages and assumptions. Real-world results vary. This information is for education only and not personal financial advice. Talk to a qualified financial advisor before making decisions.

Educational only. The information on seniortownhall is provided for general educational purposes and is not financial, legal, tax, medical, insurance, or investment advice. Rules (e.g., Social Security, Medicare, tax law) change frequently and may have changed since publication.

Please consult a qualified professional who can consider your individual circumstances before acting on any information.

© 2026 seniortownhall. All rights reserved.